Wise H1 FY26: investment flywheel or cost catch-up?

Wise’s interim results for the six months ended 30 September 2025 show a business that is still compounding on usage, while deliberately (or necessarily) leaning into a heavier cost base. Revenue rose 11%, but administrative expenses increased 27%, and profit for the period fell 14%.

The headline question remains: is Wise scaling costs as an intentional enabler of its next growth leg, or “catching up” on infrastructure, servicing, and regulatory requirements that become unavoidable at scale?

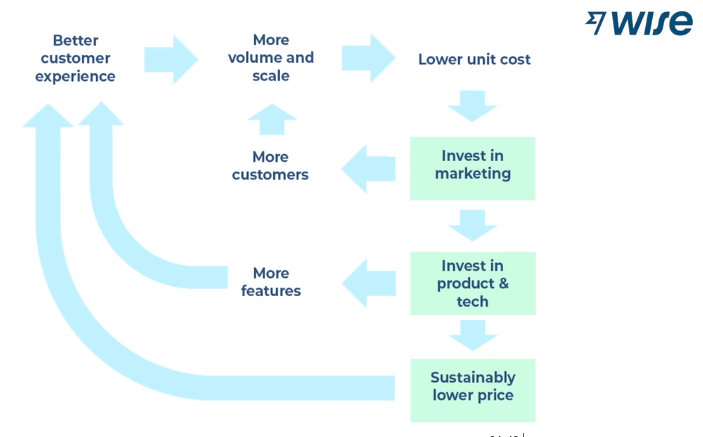

The flywheel is working but pricing makes the revenue line look slower

Wise continues to run its core playbook: grow customers, drive volume, improve speed and reliability, and use efficiency gains to lower prices over time.

From the H1 results:

Take rate 52bps -10bps (or –16%)

This drove:

Active customers 13.4m +18%

Total cross border volumes £85bn +24%

Spend on Wise cards £28bn +27%

Customer holdings £25bn +37%

Own cash on the balance sheet £1.6bn +49%

Wise Platform volumes £4.2bn +55%

However, Cross-border revenue is up only 5% YoY, despite volumes up 24%

Wise’s 52bps take rate creates a clear revenue headwind: it earns less per £ transferred, so revenue will typically grow more slowly than volumes. Importantly, the peer chart suggests this isn’t a one-off pricing move. Wise has long competed at a structurally lower take rate than incumbents.

The key question is therefore not whether Wise is “discounting” vs last year, but whether its scale, product breadth and unit-cost advantages allow it to sustain this low-price position while still expanding margins over time.

Growth is becoming broader than transfers

Wise is steadily diversifying away from “pure transfers” and toward a wider account-led ecosystem:

- Card and other revenue grew 26% YoY

- Management notes non-cross-border revenue was 41% of underlying income in the period, which supports the idea that Wise is building multiple growth engines rather than relying on one fee stream.

This matters because an account relationship (balances, card usage, platform integrations) tends to improve retention and lifetime value versus single-use transfers.

Infrastructure and distribution are expanding (and they cost money)

Wise is emphasising “network” advantages: deeper payment rail access, more instant payments, and more regulatory coverage.

In H1, it highlighted:

- Direct participation in 7 domestic payment systems (with Pix in Brazil live and Zengin in Japan expected imminently)

- Regulatory approvals from the Central Bank of the UAE to bring products to the country

- Continued product expansion (e.g., Travel Hub, under-18 accounts, and Wise Assets rollout in Brazil)

These are strategically important, but they also naturally bring higher ongoing costs: engineering, operations, compliance, and customer servicing.

Why profits fell

Management’s narrative is that last year’s unusually high margin is being reinvested, and margins are being guided back toward the medium-term framework.

They explicitly flag investment into infrastructure, products, marketing, and servicing, alongside costs linked to the planned US dual listing (which they treat as one-off).

At face value, you can tell two stories from the same numbers:

- “Intentional investment” story: Wise is choosing to spend now (team, product, marketing, rails, partnerships) to strengthen the moat and widen distribution with payback coming through higher customer growth, deeper account adoption, and eventual operating leverage.

- “Catch-up” story: Wise is being forced to raise its cost base to meet the operational and regulatory bar of a much larger, more complex global financial network because it has underinvested historically. This is essential, but potentially less value-accretive scenario.

In my next article, I’ll take a clear view on which of these is really happening (in my opinion), and what that implies for future margins, unit economics, and valuation.